The continuing diversity of corporate governance: Theories of convergence and variety

- abstract

This paper examines the continuing diversity of corporate governance by critically analysing the impelling financial forces for convergence, and the vitality of institutional differentiation. Competing theories of convergence and diversity are examined through the disciplinary perspectives of history and politics, law and regulation, culture, and institutional complementarities. The paper challenges whether a universal corporate governance system is practical, necessary or desirable. The increasingly recognised premium for governance is considered in the context of a globalising economy. The implications of the deregulation of finance and the globalisation of capital markets are examined, with a focus on the growth of equity markets and the dominant position of the Anglo-American stock exchanges. The convergence thesis is debated, examining different theoretical arguments for and against the inevitability of convergence of corporate governance systems and the resilience of cultural and institutional diversity. This institutional diversity serves a productive purpose in contributing innovation and differentiation in products and services. The global financial crisis has shaken the institutional foundations of all advanced economies, and regulatory and market settlements are still occurring. In this context of forces impelling dramatic change yet encountering powerful impulses towards institutional continuity, the future direction of corporate governance trends is questioned, with the likelihood of greater complexity rather than uniformity emerging from current developments. While capital markets have acquired an apparently irresistible force in the world economy, it still appears that institutional complementarities at the national and regional level represent immovable governance objects. The issues are more complex than convergence theorists suggest, and while some degree of market convergence might be occurring, simultaneously there is the creation of greater divergence within national regimes of corporate governance.

Introduction

This paper examines the continuing diversity of corporate governance by critically analysing the impelling financial forces for convergence, and the vitality of institutional differentiation. Convergence implies the increasing adoption by all governance systems throughout the world of a common set of institutions and practices, portrayed as an ideal rational/legal system, but invariably resting upon a belief in the virtue of market based relationships, and the associated paradigms of the prevailing Anglo-American economic and legal orthodoxy, which insists the creation of shareholder value is the ultimate objective of corporate existence. By contrast institutional differentiation approaches recognise the ongoing vitality of differentiation in the institutions, policies and practices of corporate governance, how this reflects differences in culture, values and conceptions of corporate purpose, and why this contributes to quality and variety in regional industries and products.

Competing theories of convergence and diversity are examined through the disciplinary perspectives of history and politics, law and regulation, culture, and institutional complementarities. A central thesis of the analysis is the increasing intensification of the financialisation of the global economy, which translates for corporations into an enveloping regime of maximising shareholder value as the primary objective. These financial pressures may have originated in the Anglo-American world, and are manifest in the vast international scale and penetration of Anglo-American financial institutions, however similar developments are becoming insistent in Europe, the Asia Pacific, and throughout the emerging economies. Yet diversified governance institutions confronted by these continuous pressures for international convergence have proved resilient and viable. The conclusion of the analysis is that this differentiation is valuable since different governance systems are better at doing different things, as revealed in the relative strengths and weaknesses in governance, investment strategy, and product specialization. In practice there may simultaneously be a dual dynamic of convergence and divergence taking place, where corporations learn to live with some of the pressures of international financial markets, yet value the differentiation of their regional cultures and institutions, while they strive to maintain and enhance the distinctiveness of their corporate objectives.

Indeed a fatal flaw of the convergence thesis is the assumption that some uniform, homogenized, corporate governance system would in all circumstances prove superior both functionally and institutionally than the present diversified system. In fact as a result of the differences in corporate governance structure and objectives, the different governance systems demonstrate unique strengths and weaknesses: they are good at doing different things, and they all have different problems to deal with (Clarke and Bostock, 1994; Moerland, 1995; Coombes and Watson, 2000; Dore, 2000; Clarke, 2011; Clarke and Branson, 2012; Clarke, 2016a). Anglo-American governance systems support a dynamic market orientation with fluid capital which can quickly chase market opportunities wherever they occur. This agility, ready availability of capital, intelligence and speed has enabled the US to capitalize on fast moving industries including media, software, professional services and finance in an industrial resurgence that temporarily reasserted US economic ascendancy. The weakness of this system is the corollary of its strength: the inherent volatility, short-termism and inadequate governance procedures that have often led to corporate disasters and have caused periodic financial crises (Clarke, 2013). Adopting a different orientation European enterprise as typified by the German governance system has committed to long term industrial strategies supported by stable capital investment and robust governance procedures that build enduring relationships with key stakeholders (Cernat, 2004; Lane, 2003). This was the foundation of the German economic miracle that carried the country forward as one of the leading exporters in the world of goods renowned for their exceptional quality and reliability including luxury automobiles and precision instruments. Again the weaknesses of this system are the corollary of its strengths: the depth of relationships leading to a lack of flexibility in pursuing new business opportunities in new industries and internationally. It should be noted that the German system of governance is typical of the coordinated market economies (Japan, Sweden, and Germany) of Northern Europe that have concentrated ownership and overall cooperative relations with employees compared to the mixed market Latin economies (France, Italy and Spain) which also have concentrated ownership but more conflictual relations between employers and employees (Goyer and Jung, 2011; Hancké et al., 2007; Hancké, 2009). In Asia corporate governance systems are the most networked of all, with the firm at the centre of long and enduring economic relationships with investors, employees, suppliers and customers (Claessens and Fan, 2002). This insider approach has yielded the longest investment horizons of all, and was for example the key to Japanese success in dominating overseas markets in the US and Europe with advanced electronic consumer goods, as well as in affordable quality automobiles. More recently the capacity for investing in the long term has seen the entrance onto the world stage of impressive Chinese corporations such as the Industrial and Commercial Bank of China as the world’s largest bank by assets, and Huawei as one of the world’s leading telecommunications manufacturers. However just as the weak and secretive corporate governance practices of Japan ultimately led to the bursting of the Japanese bubble in the early 1990s, and to successive governance problems since, so too the apparently inexorable rise of Chinese enterprise is threatened by covert governance and lack of transparency and accountability in finance.

A more realistic perspective than the convergence thesis is a more nuanced understanding that despite the financial and other market pressures towards convergence there will continue to be considerable diversity in the forms of corporate governance developing around the world. Different traditions, values and objectives will undoubtedly continue to produce different outcomes in governance, which will relate closely to the choices and preferences people exercise in engaging in business activity. If there is convergence of corporate governance, it could be to a variety of different forms, and it is likely there will be divergence away from the shareholder oriented Anglo-American model, as there will be convergence towards it. There is a growing realisation that shareholder value is a debilitating ideology which is undermining corporations with an over-simplification of complex business reality, weakening managers, corporations and economies, and ignoring the diversity of investment institutions and interests (Clarke, 2014; Clarke, 2015; Lazonick, 2014). Moreover the convergence ‘one-size-fits-all’ approach studiously denies the essential entrepreneurship and creativity involved in business endeavour that will continuously give rise to innovative and dynamic forms of corporate governance as we are presently seeing in new forms of social enterprise, B-corporations, and other business ventures which in turn create and develop new complementary institutions.

A universal corporate governance system?

In the contest between three resolutely different approaches to corporate governance in the Anglo-American, European and Asia-Pacific models, the question arises: is one system more robust than the others and will this system prevail and become universal? The answer to this question appeared straightforward in the 1990s. The US economy was ascendant, and the American market-based approach appeared the most dynamic and successful. Functional convergence towards the market-based system seemed to be occurring inexorably driven by forces such as:

- Increasingly massive international financial flows which offered deep, liquid capital markets to countries and companies that could meet certain minimum international corporate governance standards.

- Growing influence of the great regional stock exchanges, including the NYSE and NASDAQ, London Stock Exchange, and Euronext – where the largest corporations in the world were listed regardless of their home country.

- Developing activity of ever-expanding Anglo-American based gargantuan institutional investors, advancing policies to balance their portfolios with increasing international investments if risk could be mitigated.

- Expanding revenues and market capitalization of multinational enterprises (often Anglo-American corporations, invariably listed on the New York Stock Exchange even if European-based), combined with a sustained wave of international mergers and acquisitions from which increasingly global companies were emerging.

- Accelerating convergence towards international accounting standards; and a worldwide governance movement towards more independent auditing standards, and rigorous corporate governance practices.

Together these forces have provoked one of the liveliest debates of the last two decades concerning the globalisation and convergence of corporate governance (Roe, 2000; Hansmann and Kraakman, 2001; Branson, 2001; McDonnell, 2002; McCahery et al., 2002; Roe, 2003; Aguilera and Jackson, 2003; Gunter and van der Hoeven, 2004; Lomborg, 2004; Jesovar and Kirkpatrick, 2005; Hamilton and Quinlan, 2005; Jacoby, 2007; Deeg and Jackson, 2007; Williams and Zumbansen, 2011; Aguilera et al., 2012; Jackson and Deeg, 2012; Jackson and Sorge, 2012; Clarke, 2014; Clarke 2016a). As functional convergence proceeds in the way corporate access to finance and governance practices become universal, it is assumed that institutional convergence of legal and regulatory bodies, and governance institutions will become identical. How high the stakes are in this debate is revealed by Gordon and Roe:

Globalization affects the corporate governance reform agenda in two ways. First, it heightens anxiety over whether particular corporate governance systems confer competitive economic advantage. As trade barriers erode, the locally protected product marketplace disappears. A country’s firms’ performance is more easily measured against global standards. Poor performance shows up more quickly when a competitor takes away market share, or innovates quickly. National decision makers must consider whether to protect locally favored corporate governance regimes if they regard the local regime as weakening local firms in product markets or capital markets. Concern about comparative economic performance induces concern about corporate governance. Globalization’s second effect comes from capital markets’ pressure on corporate governance. […] Despite a continuing bias in favor of home-country investing, the internationalization of capital markets has led to more cross-border investing. New stockholders enter, and they aren’t always part of any local corporate governance consensus. They prefer a corporate governance regime they understand and often believe that reform will increase the value of their stock. Similarly, even local investors may make demands that upset a prior local consensus. The internationalization of capital markets means that investment flows may move against firms perceived to have suboptimal governance and thus to the disadvantage of the countries in which those firms are based. (2004: 2)

In the inevitable contest between the insider, relationship-based, stakeholder-oriented corporate governance system and the outsider, market- based, shareholder value-oriented system, it is often implied that the optimal model is the dispersed ownership with shareholder foci for achieving competitiveness and enhancing any economy in a globalised world. The OECD, World Bank, IMF, Asian Development Bank and other international agencies, while they have recognised the existence of different governance systems and suggested they would not wish to adopt a one-size-fits-all approach, have nonetheless consistently associated the rules-based outsider mode of corporate governance with greater efficiency and capacity to attract investment capital, and relegated the relationship-based insider mode to second best, often with the implication that these systems may be irreparably flawed. The drive towards functional convergence was supported by the development of increasing numbers of international codes and standards of corporate governance.

The vast weight of scholarship, led by the financial economists, has reinforced these ideas to the point where they appeared unassailable at the height of the new economy boom in the US in the 1990s (which coincided with a long recession for both the leading exponents of the relationship-based system, Japan and Germany), supporting the view that an inevitable convergence towards the superior Anglo-American model of corporate governance was occurring. This all appeared an integral part of the irresistible rise of globalisation and financialisation that was advancing through the regions of the world in the late 1990s and early 2000s, with apparently unstoppable force. Economies, cultures and peoples increasingly were becoming integrated into global markets, media networks, and foreign ideologies in a way never before experienced. It seemed as if distinctive and valued regional patterns of corporative governance would be absorbed just as completely as other cultural institutions in the integrative and homogenising processes of globalisation. The increasing power of global capital markets, stock exchanges, institutional investors, and international regulation would overwhelm cultural and institutional differences in the approach to corporate governance.

Yet just as there are many countries that continue to value greatly the distinctions of their culture and institutions they would not wish to lose to any globalised world, people also believe there are unique attributes to the different corporate governance systems they have developed over time, and are not convinced these should be sacrificed to some unquestioning acceptance that a universal system will inevitably be better. The field of comparative corporate governance has continued to develop however, and a different and more complex picture of governance systems is now emerging. The objectives of corporate governance are more closely questioned; the qualities of the variety and relationships of different institutional structures are becoming more apparent; the capability and performance of the different systems more closely examined; and different potential outcomes of any convergence of governance systems realised. While capital markets have acquired an apparently irresistible force in the world economy, it still appears that institutional complementarities at the national and regional level represent immovable objects (Jacoby, 2007; Deeg and Jackson, 2007; Williams and Zumbansen, 2011; Jackson and Deeg, 2012; Clarke, 2014; Clarke 2016a). This is not to argue the immutability of institutions which of course are continuously engaged in complex processes of creation, development and reinvention in the economic, social and cultural context in which they exist. However, what is at issue is the causation and direction of these institutional changes. From the convergence perspective they are a logical result of adopting the superior Anglo-American institutions of corporate governance and financial markets. From the perspective of those who respect and understand the reasons for institutional diversity and value the outcomes of this diversity, institutional change is a more autonomous process embedded within economies and societies, which may indeed have to negotiate some settlement with international market forces, but strive to do so while maintaining their own values.

An apparent third possibility to the two polar positions of convergence/institutional diversity is recognised by Coffee (2000; 2001) and Gilson (2000). Coffee (2000: 5) distinguishes ‘functional convergence’ (similarities in activities and objectives) from ‘formal convergence’ (common legal rules and institutions) and contends that functional substitutes may provide alternative means to the same ends (for example, a European company with weak investor protection and securities markets could list on the London or New York exchanges with rules that require greater disclosure of information, providing a framework of protections for minority shareholders not available in civil law countries). Coffee argues that while the law matters, legal reforms follow rather than lead market changes. Gilson (2000: 10) offers a more robust view of the force of functional convergence:

Path dependency, however, is not the only force influencing the shape of corporate governance institutions. Existing institutions are subject to powerful environmental selection mechanisms. If existing institutions cannot compete with differently organized competitors, ultimately they will not survive. Path dependent formal characteristics of national governance institutions confront the discipline of the operative selection mechanisms that encourage functional convergence to the more efficient structure and, failing that, formal convergence as well.

This view from Columbia University Law School of the ascendancy of functional governance in Europe and elsewhere, might have carried more weight if Coffee had not concluded his 2000 paper with a celebration of Germany’s rapidly growing Neuer Markt as the ‘clearest example’ of self-regulatory alternative functional governance creating a greater constituency for open and transparent markets. In fact, Germany’s Neuer Markt launched as Europe’s answer to the Nasdaq in 1997, collapsed with a precipitous decline in market value and numerous bankruptcies in 2003, leaving the question of how innovative German firms could enter the public equity markets unresolved (Burghof and Hunger, 2003). As von Kalckreuth and Silbermann (2010) state, this represented ‘[t]he spectacular rise and fall of the first and most important European market for hi-tech stocks. Given investors’ frenzy, the Neuer Markt was a special kind of natural experiment’. For some time, financing constraints were virtually non-existent, but as occurred, ‘faulty valuation by stock markets may directly induce destructive corporate behaviour: slack, empire building, excessive risk-taking, and fraud’ (ibid.). While more viable illustrations of functional convergence could readily be found, it could be argued that this approach is largely another route to the convergence thesis rather than an alternative. Indeed, functional convergence, since it is easier to achieve than institutional convergence, could prove a quicker route to shareholder value orientations.

Globalisation of capital markets

The convergence thesis is derived essentially from the globalisation thesis: that irresistible market forces are impelling the integration of economies and societies. Globalisation represents a profound reconfiguration of the world economy compared to earlier periods of internationalization. ‘An international economy links distinct national markets: a global economy fuses national markets into a coherent whole.’ (Kubrin, 2002: 7; Clarke and dela Rama, 2006). A major driver of the globalisation phenomenon has proved the massive development of finance markets, and their increasing influence upon every other aspect of the economy:

Financial globalisation, i.e. the integration of more and more countries into the international financial system and the expansion of international markets for money, capital and foreign exchange, took off in the 1970s. From the 1980s on, the increase in cross-border holdings of assets outpaced the increase in international trade, and financial integration accelerated once more in the 1990s… The past decade has also seen widespread improvements in macroeconomic and structural policies that may to some extent be linked to a disciplining effect of financial integration. Moreover, there is evidence that financial linkages have strengthened the transmission of cyclical impulses and shocks among industrial countries. Financial globalisation is also likely to have helped the build-up of significant global current account imbalances. Finally, a great deal of the public and academic discussion has focussed on the series of financial crises in the 1990s, which has highlighted the potential effects of capital account liberalisation on the volatility of growth and consumption. (European Commission, 2005: 19)

The complex explanation for this massive financialisation of the world economy is pieced together by Ronald Dore thus:

- Financial services take up an ever larger share of advertising, economic activity and highly skilled manpower.

- Banks respond to the decline in loan business with a shift to earning fees for financial and investment services and own account trading.

- Shareholder value is preached as the sole legitimate objective and aspiration of corporations and executives.

- Insistent and demanding calls for ‘level playing fields’ from the World Trade Organisation and Bank of International Settlements (BIS), with pressures for the further liberalisation of financial markets, and greater international competition forcing international financial institutions, and other corporations to work within the same parameters. (Dore, 2000: 4-6)

What is resulting from this insistent impulse of the increasingly dominant financial institutions are economies (and corporations) increasingly dependent upon financial markets:

Global integration and economic performance has been fostered by a new dynamic in financial markets, which both mirrors and amplifies the effects of foreign direct investment and trade driven integration. The economic performance of countries across the world is increasingly supported by – and dependent on – international capital flows, which have built on a process of progressive liberalisation and advances in technology since the 1980s’ (European Commission, 2005: 8).

Financial innovations and financial cycles have periodically impacted substantially on economies and societies, most notably in the recent global financial crisis (Rajan, 2010; Clarke, 2010a). However the new global era of financialisation is qualitatively different from earlier regimes. Global finance is now typified by a more international, integrated and intensive mode of accumulation, a new business imperative of the maximisation of shareholder value, and a remarkable capacity to become an intermediary in every aspect of daily life (van der Zwan, 2013). Hence finance as a phenomenon today is more universal, aggressive and pervasive than ever before (Krippner, 2005; 2012; Epstein, 2005; 2015; Dore, 2008; Davis, 2009; van der Zwan, 2013). These financial pressures are translated into the operations of corporations through the enveloping regime of maximising shareholder value as the primary objective. Agency theory has provided the rationale for this project, prioritizing shareholders above all other participants in the corporation, and focusing corporate managers on the release of shareholder value incentivized by their own stock options. In turn this leads to an obsessive emphasis on financial performance measures, with increasingly short term business horizons (Lazonick, 2012; 2014; Clarke, 2013; Clarke, 2015).

The growth of international equity markets

A vital dimension of the increasing financialisation of the world economy is the growth of capital markets, and especially the vast growth of equity markets, where volatility has been experienced at its furthest extremities. What this demonstrates is the overwhelming predominance of Anglo-American institutions and activity in world equity markets, and how to a great extent these markets reflect largely Anglo-American interests, as the rest of the world depends more on other sources of corporate finance. This pre-eminence of equity markets is a very recent phenomenon. Historically, the primary way most businesses throughout the world (including in the Anglo-American region) have financed the growth of their companies is internally through retained earnings. In most parts of the world until recently, this was a far more dependable source of capital rather then relying on equity markets. Equity finance has proved useful at the time of public listing when entrepreneurs and venture capitalists cash in their original investment, as a means of acquiring other companies, or providing rewards for executives through stock options. Equity finance is used much less frequently during restructuring or to finance new product or project development (Lazonick, 1992: 457). In Europe and the Asia-Pacific however, this capital was in the past provided by majority shareholders, banks, or other related companies (to the extent it was needed by companies committed to organic growth rather than through acquisition, and where executives traditionally were content with more modest personal material rewards than their American counterparts).

The euphoria of the US equity markets did reach across the Atlantic with a flurry of new listings, which formed part of a sustained growth in the market capitalisation of European stock exchanges as a percentage of GDP. A keen attraction of equity markets for ambitious companies is the possibility of using shares in equity swaps as a means of taking over other companies thus fuelling the take-over markets of Europe. This substantial development of the equity markets of France, the Netherlands, Germany, Spain, and Belgium and other countries began to influence the corporate landscape of Europe, and was further propelled by the formation of Euronext, and the subsequent merger with the NYSE. Indeed, as the regulatory implications of Sarbanes Oxley emerged in the United States from 2003 onwards, the market for IPOs moved emphatically towards London, Hong Kong and other exchanges. Concerned about the impact of Sarbanes Oxley on the US economy a group of authorities formed the Committee on Capital Markets Regulation highlighted the damage being caused to what for many years was recognised as ‘the largest, most liquid, and most competitive public equity capital markets in the world’ (CCMR, 2006: ix). Though the US total share of global stock market activity remained at 50 per cent in 2005, the IPO activity had collapsed. From attracting 48 per cent of global IPOs in the late 1990s, the US share dropped to 6 per cent in 2005, when 24 of the 25 largest IPOs were in other countries (CCMR, 2006: 2). The more relaxed regulatory environment of the UK and other jurisdictions clearly for a time at least proved attractive in an ongoing process of international regulatory arbitrage.

This greater vibrancy in European markets partly explains the NYSE’s interest in merging with Euronext, and the NASDAQ’s long but failed courtship with the London Stock Exchange. Any such mergers represent a further US bridgehead into the equity markets of Europe, rather than the converse. Along with the growth in market capitalisation in European exchanges occurred a gradual increase also in trading value. It appears that contemporary equity markets inevitably will be associated with high levels of trading activity, as a growing proportion of trading is algorithmic high frequency computer generated. Following the global financial crisis, regulatory intervention in finance was perceived to be more robust in Europe and the UK, and less so in the United States (with the slow pace of the introduction of the monumental Dodd-Frank Act). In this context the attractions of the New York Stock Exchange and Nasdaq returned, and by 2014 reached once again the levels of IPO financing in the dot-com 1990s era, far exceeding the amounts raised in the London and Hong Kong markets combined (Financial Times, 29 September 2014).

The important role of equity markets in fostering further international financial integration was recognised by the European Commission (2005): ‘Globally, portfolio investment is the largest asset category held cross-border; global portfolios (equity and debt securities) amounted to 19 trillion US dollar at the end of 2003 (IMF CPIS, preliminary data)’. As equity markets come to play a more powerful role in corporate life in Europe, Japan and other parts of the world, a set of assumptions and practices are also disseminated which may confront long standing values and ideals in the economies and societies concerned. Specifically, the ascendancy of shareholder value as the single legitimate objective of corporations and their executives, usually accompanies increasing dependence upon equity markets. Dore (2000) cites a Goldman Sachs study of manufacturing value added in the United States, Germany and Europe in general, which concluded that:

The share of gross value added going to wages and salaries has declined on trend in the US since the early 1980s. In fact, for the US, this appears to be an extension of a trend that has been in place since the early 1970s… We believe that the pressures of competition for the returns on capital available in the emerging economies have forced US industry to produce higher returns on equity capital and that their response to this has been to reserve an increasingly large share of output for the owners of capital. (Young, 1997)

This insistent pressure to drive increases in capital’s returns at the expense of labour inherent in Anglo-American conceptions of the nature of equity finance is roundly condemned by Dore as the negation of essential values previously considered central to economic good in both Europe and Japan:

Multiple voices are urging Japanese managers to go in the same direction. The transformation on the agenda may be variously described – from employee sovereignty to shareholder sovereignty: from the employee-favouring firm to the shareholder-favouring firm; from pseudo-capitalism to genuine capitalism. They all mean the same thing: the transformation of firms run primarily for the benefits of their employees into firms run primarily, even exclusively, for the benefit of their shareholders… It means an economy centred on the stock market as the measure of corporate success and on the stock market index as a measure of national well-being, as opposed to an economy which has other, better, more pluralistic criteria of human welfare for measuring progress towards the good society. (2000: 9-10)

The euphoric enthusiasm for the power of equity markets was severely dented by the Enron/WorldCom series of corporate collapses in the US. With about seven trillion dollars wiped off the New York stock exchange in 2001/2002, and the executives of many leading corporations facing criminal prosecution, the recovery in equity markets came sooner and more robustly than expected. However part of the price of restoring confidence to the markets was the hasty passage of the Sarbanes Oxley legislation and increased regulation of corporate governance.

Yet Sarbanes Oxley apparently did little to curb the animal spirits of some fringes of the US financial institutions that ultimately impacted on the world economy. The subprime mortgage crisis, and the elaborate financial instruments developed to pass on risk by investment banks, that caused a prolonged implosion of financial institutions in the global financial crisis of 2007/2008 was an indication of the dangers presented by the increasing financialisation of economic activity, and the hazardous context for corporate governance in market oriented economies (Clarke, 2010a). Nonetheless despite the strenuous intervention of the G20, Financial Stability Board internationally and the Dodd-Frank legislation in the US intended to restrain the most dangerous impulses of financial institutions, the strength and vigour of capital markets seems destined to continue to advance globally without adequate regulation or oversight (Clarke and Klettner, 2011; Avgouleas, 2013).

While each of the regional systems of finance and corporate governance remains in the post-financial crisis period weakened and to a degree disoriented, the substance and rhythm of institutional varieties continues: in Germany there remains an incomplete form of market liberalization, and resilient elements of the social market economy (Jackson and Sorge, 2012); in France, while the neo-liberal reforms have undermined social alliances and the pressures for institutional change increase, social commitments continue (Amable et al., 2012); and in Japan the incursions of hedge funds and private equity with a growing proportion of overseas ownership of Japanese corporations has not deflected Japanese executives from maintaining more inclusive conceptions in their definition of corporate purpose (Seki and Clarke, 2014).

Convergence and diversity of corporate governance

Despite the recurrent crises originating in Anglo-American finance and governance in this period, and in the background the continuing reverberations of the global financial crisis, the confidence the market based system was the only way forward has continued almost undaunted in government and business circles, certainly in the Anglo-American world (Clarke, 2010a). Underlying the resurging energy of advancing equity markets and the proliferating corporate governance guidelines and policy documents appearing in such profusion over the last two decades is an implicit but confident sense that an optimal corporate governance model is indeed emerging:

An optimal model with dispersed ownership and shareholder foci… The OECD and World Bank promote corporate governance reform… Influenced by financial economists and are generally promoting market capitalism with a law matters approach, although for political reasons, they do not advocate too strongly market capitalism and allow for other corporate governance systems (i.e. concentrated ownership). (Pinto, 2005: 26-7)

Other authorities are less diplomatic in announcing the superiority of the Anglo-American approach that other systems must inevitably converge towards. Two US eminent law school professors Hansmann and Kraakman in an article prophetically entitled The end of history for corporate law led the charge of the convergence determinists:

Despite very real differences in the corporate systems, the deeper tendency is towards convergence, as it has been since the nineteenth century. The core legal features of the corporate form were already well established in advanced jurisdictions one hundred years ago, at the turn of the twentieth century. Although there remained considerable room for variation in governance practices and in the fine structure of corporate law throughout the twentieth century, the pressures for further convergence are now rapidly growing. Chief among these pressures is the recent dominance of a shareholder-centred ideology of corporate law among the business, government and legal entities in key commercial jurisdictions. There is no longer any serious competitor to the view that corporate law should principally strive to increase long-term shareholder value. This emergent consensus has already profoundly affected corporate governance practices throughout the world. It is only a matter of time before its influence is felt in the reform of corporate law as well. (2001: 1)

The irony of this profoundly ideological claim (the most recent in a long historical lineage of similar appeals), is that it attempts to enforce the consensus it claims exists, by crowding out any possibility of alternatives. This is not an isolated example, but the dominant approach of much legal and financial discussion in the United States, where as McDonnell insists the prevailing view is:

The American system works better and that the other countries are in the process of converging to the American system. Though there is some dissent from this position, the main debate has been over why countries outside the United States have persisted for so long in their benighted systems and what form their convergence to the American way will take. The scholarly discussion has converged too quickly on the convergence answer. (2002: 2)

It is worth asking by what standards or criteria a system of corporate governance may be defined as ‘optimal’? Where a definition is offered in the convergence literature for an optimal corporate governance system it invariably relates to accountability to shareholders, and often to maximising shareholder value which became an increasingly insistent ideology in Anglo-American analyses of corporate purpose. The narrow financial metrics relating to maximising shareholder value often are presented as the only valid measures of an optimal corporate governance system, when there are deeper and wider measures that could be employed in the estimation of business performance.

Business success might be measured in longevity, scale, revenue, sales, employment, product quality, customer satisfaction, or many other measures that might be found relevant in different societies at different times. Certainly the measures of business success employed in Europe and Asia are quite different from the Anglo-Saxon world, and would embrace wider stakeholder interests. Most economic analyses simply substitute ‘efficient’ for optimal, but McDonnell (2002) offers three relevant values:

- efficiency

- equity

- participation

In considering efficiency there is the question of how well the governance system solves agency problems; how well the system facilitates large scale coordination problems; how well the systems encourage long-term innovation; and how they impose different levels of risk on the participants. Distributional equity is another important value, but again is difficult to measure. For many distributional equity suggests increased prosperity should provide for an increased equality of income and wealth, but others find this less compelling. In some instances, equity may conflict with efficiency: it could be argued the US system is more efficient, but inevitably results in greater inequality. Alternatively equity may be associated with more collaborative creativity. Finally there is the value of participation, both in terms of any contribution this may make to the success of the enterprise, and as an end in itself in enhancing the ability and self-esteem of people. Corporate governance systems affect the level of participation in decision-making very directly, whether encouraging or disallowing active participation in enterprise decision-making (McDonnell, 2002: 4).

Arguably each of these values is of great importance, and the precise balance between them is part of the choice of what kind of corporate governance system is adopted. Yet there appears increasingly less opportunity to exercise this choice:

The universe of theoretical possibilities is much richer than a dominant strand of the literature suggests, and we are currently far short of the sort of empirical evidence that might help us sort out these possibilities. Most commentators have focused on efficiency to the exclusion of other values. Moreover, even if convergence occurs, there is a possibility that we will not converge on the best system. Even if we converge to the current best system, convergence still may not be desirable. (McDonnell, 2002: 2)

History and politics

In the past these critical political choices on which system of governance provides the most value in terms of efficiency, equity and participation have been made and defended. Mark Roe’s (2000; 2003) path dependence thesis rests on how political forces in America, anxious about the influence of concentrated financial or industrial monopolies, resisted any effort at concentration of ownership or ownership through financial institutions, resulting in dispersed ownership. In contrast European social democracy has tended to favour other stakeholder interests, particularly labour, as a system that promotes welfare among all citizens and attempts to prevent wide disparities. In turn this can be viewed as a reaction to the historical rise of fascism and communism (Pinto, 2005: 22). Fligstein and Freeland (1995: 21) adopt a similar historical view that the form of governance is a result of wider political and institutional developments:

- the timing of entry into industrialisation and the institutionalisation of that process;

- the role of states in regulating property rights and the rules of competition between firms; and

- the social organisation of national elite.

In this way characteristic institutions of the US economy can be traced back to distinctive political and regulatory intervention, resulting for example in historically distributed banks, diversified companies, and the dominance of the diversified (M-form) corporations. In contrast in Europe and Japan the regulatory environment encouraged a very different approach:

Regulatory policy in the United States had the unintended consequence of pushing U.S. companies in the direction of unrelated diversification, whereas in Germany and Japan it continued on a pre-war trajectory of discouraging mergers in favour of cartels and of promoting corporate growth through internal expansion rather than acquisitions. In other words, modern regulatory policy in the U.S. produced corporations who relied on markets to acquire ideas and talent, whereas in Germany and Japan it produced corporations whose primary emphasis was on production and on the internal generation of ideas through development of human capital and organizational learning. The implications for corporate governance are straightforward: corporations favour shareholders in the U.S. so as to obtain capital for diversification and acquisitions; they favour managers and employees in the Germany and Japan so as to create internal organizational competencies. (Jacoby, 2001: 8)

A very different reading of these events is offered by Rajan and Zingales (2003), who argue that widely dispersed shareholders is related to the development of liquid securities markets and the openness to outside investments, while it was not social democracy but protectionism that kept European and Japanese markets closed from competition with concentrated ownership. As financial economists they favour the globalisation route to open market based competition, which they see as the way to unsettling local elites, achieving dispersed ownership, raising capital, and improving corporate governance.

Law and regulation

Following a different line of analysis the substantial empirical evidence of La Porta et al. (1998; 1999; 2000; 2002) concerning countries with dispersed and concentrated ownership, which demonstrates differences in the legal protection of shareholders was very influential. Law and regulation may impede or promote convergence or divergence. In many countries without adequate laws guaranteeing dispersed shareholder rights, the only alternative appeared to maintain control through concentrated ownership. This led to the conclusion that the law determined the ownership structure and system of corporate finance and governance. Jurisdictions where the law was more protective encouraged the emergence of more dispersed ownership (Pinto, 2005: 19). Coffee (2001) extends La Porta et al.’s acceptance that in the common law system there was greater flexibility of response to new developments offering better protection to shareholders, to the argument that the critical role of the decentralised character of common law institutions was to facilitate the rise of both private and semi-private self-regulatory bodies in the US and UK. In contrast in civil law systems the state maintained a restrictive monopoly over law-making institutions (for example in the early intrusion of the French government into the affairs of the Paris Bourse involving the Ministry of Finance approving all new listings). Coffee concludes that it was market institutions that demanded legal protection rather than the other way around:

The cause and effect sequence posited by the La Porta et al. thesis may in effect read history backwards. They argue that strong markets require strong mandatory rules as a precondition. Although there is little evidence that strong legal rules encouraged the development of either the New York or London Stock Exchanges (and there is at least some evidence that strong legal rules hindered the growth of the Paris Bourse), the reverse does seem to be true: strong markets do create a demand for stronger legal rules. Both in the U.S. and the U.K., as liquid securities markets developed and dispersed ownership became prevalent, a new political constituency developed that desired legal rules capable of filling in the inevitable enforcement gaps that self-regulation left. Both the federal securities laws passed in the 1930’s in the U.S. and the Company Act amendments adopted in the late 1940's in the U.K. were a response to this demand (and both were passed by essentially “social democratic” administrations seeking to protect public securities markets). Eventually, as markets have matured across Europe, similar forces have led to the similar creation of European parallels to the SEC. In each case, law appears to be responding to changes in the market, not consciously leading it. (Coffee, 2001: 6)

Culture – Deep causation

In the search for explanations some have attempted a philosophical approach including Fukuyama (1996) who conceives of business organisations as the product of trust, and the different governance systems as built of different forms of trust relations. Regarding the social foundations and development of ownership structures and the law, other writers have examined the correlations between law and culture. Licht (2001) examines the relevance of national culture to corporate governance and securities regulation, and explores the relationship between different cultural types and the law:

A nation’s culture can be perceived as the mother of all path dependencies. Figuratively, it means that a nation’s culture might be more persistent than other factors believed to induce path dependence. Substantively, a nation’s unique set of cultural values might indeed affect – in a chain of causality – the development of that nation’s laws in general and its corporate governance system in particular. (2001: 149)

In working towards a cross-cultural theory of corporate governance systems, Licht (2001) demonstrates that corporate governance laws exhibit systematic cultural characteristics.

A comparison between a taxonomy of corporate governance regimes according to legal families (‘the legal approach’) and a classification of countries according to their shared cultural values demonstrates that the legal approach provides only a partial, if not misleading, depiction of the universe of corporate governance regimes. Dividing shareholder protection regimes according to groups of culturally similar nations is informative. The evidence corroborates the uniqueness of common law origin regimes in better protecting minority shareholders. However, statutes in the English Speaking cultural region offer levels of protection to creditors similar to the laws in the Western European or Latin American regions. Our findings cast doubt on the alleged supremacy of common law regimes in protecting creditors and, therefore, investors in general. Finally, we find that analyses of corporate governance laws in Far Eastern countries, a distinct cultural region, would benefit from combining an approach that draws on cultural value dimensions and one that draws on legal families. (Licht, 2001: 32)

Licht concludes that corporations are embedded within larger socio-cultural settings in which they are incorporated and operate. Cultural values are influential in determining the types of legal regimes perceived and accepted as legitimate in any country, and serve as a guide to legislators. Hence cultural values may impede legal reforms that conflict with them and the naiveté underlying quick-fix suggestions for corporate law reform (2001: 33-4). Culture also influences what are perceived as the maximands of corporate governance – for example in the debate over stockholders’ versus stakeholders’ interests as the ultimate objective of the corporation: ‘The corporate governance problem therefore is not one of maximising over a single factor (the maximand). Rather, it calls for optimizing over several factors simultaneously’ (Licht, 2003: 5). Berglof and von Thadden (1999) suggest the economic approach to corporate governance should be generalised to a model of multilateral interactions among a number of different stakeholders. They argue that though protection of shareholder interests may be important, it may not be sufficient for sustainable development, particularly in transitional economies. Licht concludes:

Every theory of corporate governance is at heart a theory of power. In this view, the corporation is a nexus of power relationships more than a nexus of contracts. The corporate setting is rife with agency relationships in which certain parties have the ability (power) unilaterally to affect the interests of other parties notwithstanding pre-existing contractual arrangements. In the present context, corporate fiduciaries are entrusted with the power to weigh and prefer the interests of certain constituencies to the interests of others (beyond their own self-interest). Given the current limitations of economic theory, progress in the analysis of the maximands of corporate governance may be achieved by drawing on additional sources of knowledge. (Licht, 2003: 6)

Institutional complementarities

A further development of the path dependence thesis, is the emphasis on the interdependence of economic and social institutions: ‘Corporate governance consists not simply of elements but of systems… Transplanting some of the formal elements without regard for the institutional complements may lead to serious problems later, and these problems may impede, or reverse, convergence’ (Gordon and Roe, 2004: 6). Optimal corporate governance mechanisms are contextual and may vary by industries and activities. Identifying what constitutes good corporate governance practice is complex, and cannot be templated into a single form. One needs to identify the strengths and weaknesses in the system but also the underlying conditions which the system is dependant upon (Pinto, 2005: 31; Maher and Andersson, 2000). The institutions that compose the system of corporate governance and complement each other consist not just of the law, finance, and ownership structure.

Complementarities may extend to such things as labour relations and managerial incentive systems. In Germany and Japan, the corporations’ long term relations with banks, customers, and suppliers traditionally facilitates long term commitments to employees. The commitment to permanency promotes extensive firm-specific training, which contributes to flexible specialisation in the production of high quality goods. In contrast in the United States employer training investments are lower than in Japan and Germany, employees are more mobile, and there is less firm-specific skill development. Similarly, in the US fluid managerial labour markets make it easier for ousted managers to find new jobs after a hostile takeover. In contrast, in Japan management talent is carefully evaluated over a long period of time through career employment and managerial promotion systems. Jacoby contends ‘It is difficult to disentangle the exogenous initial conditions that established a path from the ex post adaptations…What’s most likely to be the case is that capital markets, labour markets, legal regulations, and corporate norms co-evolved from a set of initial conditions’ (2001: 17). He continues with a warning to those who might wish to randomly transplant particular institutional practices into other countries:

Given institutional complementarities and path dependence, it’s difficult for one country to borrow a particular practice and expect it to perform similarly when transplanted to a different context…Were the Japanese or Germans to adopt a U.S.-style corporate governance approach that relies on takeovers to mitigate agency problems, it would prove highly disruptive of managerial incentive and selection systems presently in place. Hostile takeovers also would be disruptive of relations with suppliers and key customers, a substantial portion of which exist on a long term basis. In Germany and, especially, in Japan, there is less vertical integration of industrial companies than in the United States or the United Kingdom. Rather than rely primarily on arms-length contracts to protect suppliers and purchasers from opportunism, there is heavy use of relational contracting based on personal ties, trust, and reputation. Personal ties are supported by lifetime employment; the business relations are buttressed by cross-share holding. In short, imitation across path-dependent systems is inhibited by the cost of having to change a host of complementary practices that make an institution effective in a particular national system. (ibid.:18)

Another way of understanding this Jacoby suggests is through the concept of multiple equilibria, which leads to the conclusion there is no best way of designing institutions to support stability and growth in advanced industrial countries:

Multiple equilibria can arise and persist due to path dependence, institutional complementarities, bounded rationality, and comparative advantage. Sometimes multiple equilibria involve functionally similar but operationally distinctive institutions, such as the use of big firms as incubators in Japan versus the U.S. approach of incubation via start-ups and venture capital. Other times different institutions create qualitatively different outcomes. That is, a set of institutions, including those of corporate governance, may be better at facilitating certain kinds of business strategies and not others. Companies – and the countries in which they are embedded – can then secure international markets by specializing in those advantageous business strategies because foreign competitors will have difficulty imitating them. For example, the emphasis on specific human capital in German and Japan is supportive of production based technological learning, incremental innovation, and high quality production, all areas in which those economies have specialized. By contrast, the U.S. emphasis on resource mobility and on high short-term rewards directs resources to big-bang technological breakthroughs. In short, there are substantial gains to be reaped from sustaining institutional diversity and competing internationally on that basis. (ibid.: 25)

The discussion of corporate governance is often framed in static efficiency terms, Jacoby contends, as if it was possible to measure the comparative performance of national governance institutions in a static framework. This is inadequate for understanding the dynamic properties of governance systems, especially concerning innovation and long-term growth.

When there are multiple equilibria and bounded rationality regarding what constitutes an institutional optimum, we are operating in the world of the second best. In that world, there is no reason to believe that revamping a governance system will necessarily move an economy closer to an economic optimum. The economic case for the superiority of Anglo-American governance – and of the Anglo-American version of “free markets” as we know them, as opposed to a theoretical ideal – is actually rather weak. (ibid.: 27)

Integrated together the competing theories of convergence and diversity propounded in the disciplinary perspectives of history and politics, law and regulation, culture, and institutional complementarities offer a more nuanced prognosis of the future trends in corporate governance than crudely deterministic theories of governance convergence suggest. History and politics reminds us of the relation of distinctive institutional developments to the timing of industrialisation, the relative autonomy of states in regulating property and competition, and the significance of the structure and distribution of power and elites. Law and regulation impress upon us the significance of the distinctiveness of common and civil law approaches, and how these respond to maturing markets. Cultural approaches perceive the social foundations and distinctive values that inform different regimes of governance. Finally, the institutional complementarities approach identifies the interdependence of economic and social institutions that create complex systems of governance. These dynamic multiple equilibria of governance systems are unique, and whilst they might exhibit some degree of functional similarity, are based on profoundly distinctive experiences, values and objectives.

Different governance systems are better at doing different things

For Hansmann and Kraakman, convergence of corporate governance systems towards the shareholder-oriented model is not only desirable and inevitable, it has already happened. They boldly confirm:

The triumph of the shareholder-oriented model of the corporation over its principal competitors is now assured, even if it was problematic as recently as twenty-five years ago. Logic alone did not establish the superiority of this standard model or of the prescriptive rules that it implies, which establish a strong corporate management with duties to serve the interests of shareholders alone, as well as strong minority shareholder protections. Rather, the standard model earned its position as the dominant model of the large corporation the hard way, by out-competing during the post-World War II period the three alternative models of corporate governance: the managerialist model, the labour-oriented model, and the state-oriented model. (2001: 16)

For Hansmann and Kraakman, alternative systems are not viable competitively, only the lack of product market competition has kept them alive, and as global competitive pressures increase any continuing viability of alternative models will be eliminated, encouraging the ideological and political consensus in favour of the shareholder model.

Hansmann and Kraakman dismiss the three rivals they set up for the victorious shareholder model. The managerialist model is associated with the US in the 1950s and 1960s, when it was thought professional managers could serve as disinterested technocratic fiduciaries who would guide the business corporation in the interests of the general public. According to Hansmann and Kraakman, this model of social benevolence collapsed into self-serving managerialism, with significant resource misallocation, imperilling the competitiveness of the model and accounting for its replacement by the shareholder driven model in the US (Gordon and Roe, 2004).

The labour-oriented model exemplified by German co-determination, but manifest in many other countries, possesses governance structures amplifying the representation of labour, which Hansmann and Kraakman claim are inefficient because of the heterogeneity of interests among employees themselves, and between employees and shareholders. Firms with this inherent competition of interests would inevitably lose out in product market competition. Finally, the state-oriented model associated with France or Germany entails a large state role in corporate affairs through ownership or state bureaucratic engagement with firm managers, allowing elite guidance of private enterprise in the public interest. Hansmann and Kraakman argue this corporatist model has been discredited because of the poor performance of socialist economies (Gordon and Roe, 2004).

At the height of the NASDAQ boom when Hansmann and Kraakman wrote their visionary article it might have appeared that the shareholder model in its US manifestation was certainly globally hegemonic in all of its manifestations. However, the post-global financial crisis world is less easily convinced of the inevitable and universal superiority of the US model of governance, and Hansmann and Kraakman may have written off the prospects of Japan and Europe a little too presumptuously, the best that could be salvaged from their over-confident thesis. The Anglo-American system might be better at doing some things which require the ready deployment of large amounts of liquid capital such as in high-tech innovation and global financial services. But the other governance systems have their own dynamism and valuable capabilities such as exhibited in German precision engineering, Japanese consumer electronics, French luxury goods, or Italian design. Essentially it seems that the different corporate governance systems may be better at doing different things, and with different outcomes for the economy and society.

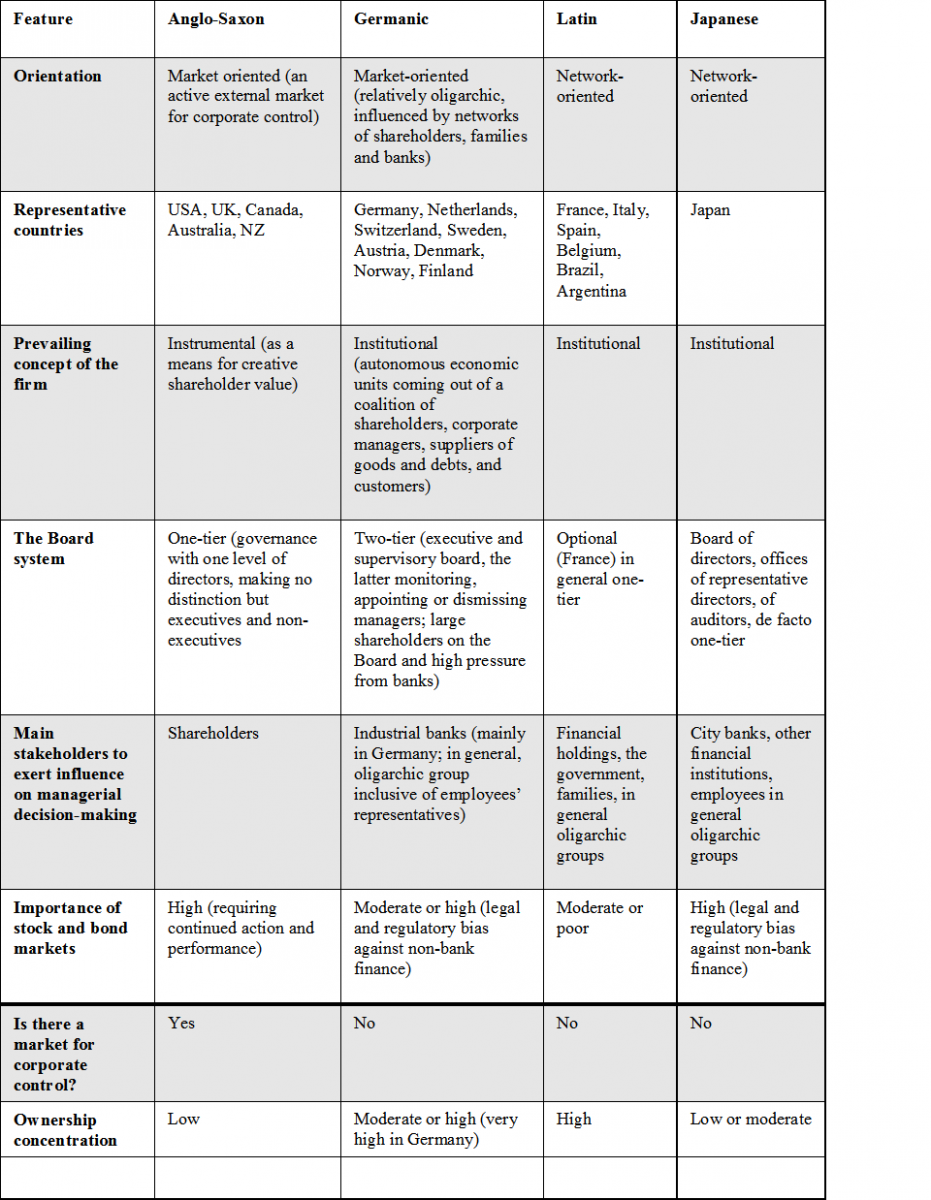

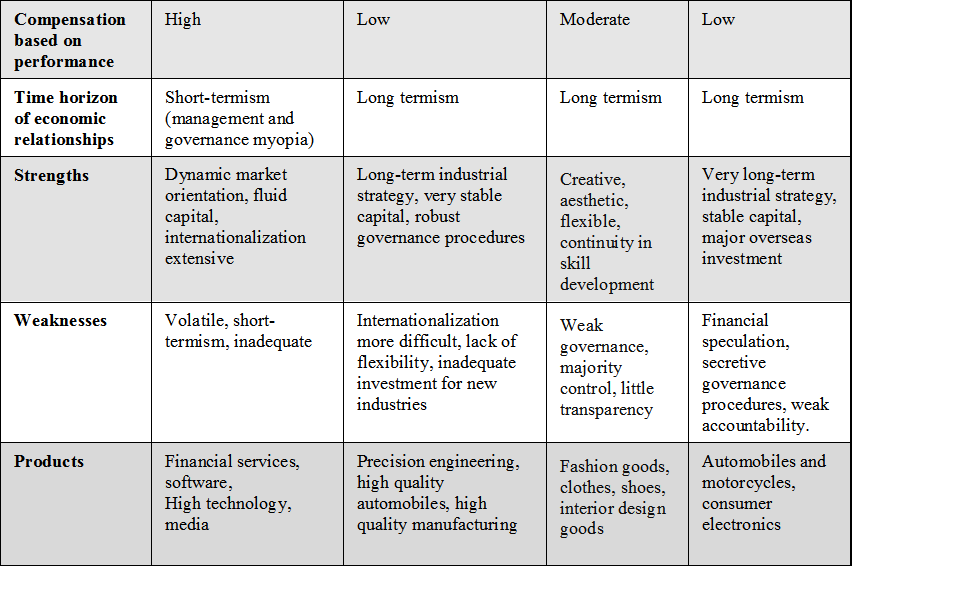

Table 1. The continuing diversity of corporate governance systems. Sources: Adapted from Keenan and Aggestam (2001); Clarke and Bostock (1994).

The continuing diversity in Anglo-American, Germanic, Latin and Japanese corporate governance systems is outlined in Table 1, indicating different orientations, concept of the firm, board structures, main stakeholders, the importance of stock and bond markets, the market for corporate control, ownership concentration, executive compensation, investment horizons, and the resulting corporate strengths and weaknesses that influence the types of products and services that are specialised in. The differences highlighted demonstrate that despite insistent pressures towards institutional and functional convergence, there remains a variety and distinctiveness in the regional approaches to corporate governance and strategy, which relates closely to their respective business strengths and weaknesses. There is a dynamism and vitality to this specialisation which continues to drive the distinctiveness and quality of the industries and products of these regions, despite the international financial, global value chain and functional pressures not only towards convergence but towards bland homogeneity in global industries, products and services.

As Douglas Branson concludes regarding the globalisation and convergence debate, ‘seldom will one see scholarship and advocacy that is as culturally and economically insensitive, and condescending, as is the global convergence advocacy scholarship that the elites in United States academy have been throwing over the transom. Those elites have oversold an idea that has little grounding in true global reality’ (2004: 276). Bebchuk and Roe’s (1999) view still holds that neither shareholder primacy nor dispersed ownership will easily converge. Path dependence has evolved established structures not easily transformed and complimentary institutions make it more difficult to do so. ‘Thus keeping existing systems may in fact be an efficient result. This lack of convergence allows for diversity and suggests that globalisation will not easily change the models’ (Pinto, 2005: 29).

A more realistic global perspective than the convergence thesis is that there will continue to be considerable diversity both in the forms of corporate governance around the world. Different traditions, values and objectives will undoubtedly continue to produce different outcomes in governance, which will relate closely to the choices and preferences people exercise in engaging in business activity. If there is convergence of corporate governance, it could be to a variety of different forms, and it is likely there will be divergence away from the shareholder oriented Anglo-American model, as there will be convergence towards it. There is a growing realisation that shareholder value is a debilitating ideology which is undermining corporations with an over-simplification of complex business reality, weakening managers, corporations and economies, and ignoring the diversity of investment institutions and interests (Clarke, 2014; Lazonick, 2014).

Certainly boards of directors in the US and UK in recent years have felt a more immediate responsibility to recognise a wider range of relevant constituencies as stakeholder perspectives arguably have once again become a more prominent part of corporate life (David et al., 2007; Deakin and Whittaker, 2007; Clarke, 2010b; Klettner et al., 2014; Clarke, 2015; Clarke, 2016b). In US firms recognition of the growing importance of intellectual capital, and the adoption of high performance work practices, have all reemphasised the importance of human capital in a context where previously labour was marginalised in the interests of a single minded shareholder ethos (Jacoby, 2001: 26). It is ironic that as European and Japanese listed corporations are being forced to recognise the importance of shareholder value; Anglo-American corporations are being sharply reminded of their social responsibilities.

The widespread adoption among leading Anglo-American corporations of publishing social and environmental reports alongside their financial reports, and actively demonstrating their corporate social responsibility in other more practical ways, suggests this may be more than simply a rhetorical change (Searcy, 2012; Schembera, 2012). The formal adoption of enlightened shareholder value in the UK Companies Act indicates at least a rhetorical move forwards from the more naked pursuit of shareholder value (Keay, 2013). Further unlikely evidence that the United States system could in some important ways be converging towards the European model is unearthed by Thomsen (2001).

The pattern of insider ownership and extensive block holding in the US, does not demarcate the American system as sharply from the European as is often suggested. And the trend may be in this direction as apparently the stock market in Anglo-American systems responds positively to higher ownership by financial institutions, and one reason for this may be the perception of better monitoring (Thomsen, 2001: 310). The increasing importance of institutional investors in the US, and in every other market, means that ownership relations are once again becoming more concentrated (even if the ultimate beneficiaries are highly diffuse). This institutional ownership has begun to create forms of relational investing, which could over time lead to more exercise of voice and less of exit by US shareholders (Jacoby, 2001: 26).

Much attention has been focussed upon the pressures driving large listed German corporations to focus more directly on the creation of shareholder value, and upon the insistent pressures for Japanese corporations to demonstrate more transparency and disclosure (Clarke and Chanlat, 2009; Jackson and Sorge, 2012; Amable et al., 2012; Seki and Clarke, 2014). Less attention has been paid to the developing pressures upon Anglo-American corporations to exercise greater accountability towards institutional investors and more responsibility in relation to their stakeholder communities (Williams and Zumbansen, 2011; Deeg, 2012).

With multiple institutions exerting interdependent effects on firm level outcomes (Aguilera and Jackson, 2003: 448), and with different values informing the objectives for the enterprise in different cultures (Hofstede, 2004), the scenario for convergence and diversity of corporate governance models is more complex and unpredictable than many commentators have suggested. A pioneer of corporate governance possessed a more compelling grasp of the possibilities that convergence and divergence may occur simultaneously: that is an insistent increase in diversity within an overall trend towards convergence:

Looking ahead towards the next decade it is possible to foresee a duality in the developing scenarios. On the one hand, we might expect further diversity – new patterns of ownership, new forms of group structure, new types of strategic alliance, leading to yet more alternative approaches to corporate governance. More flexible and adaptive organisational arrangements, entities created for specific projects, business ventures and task forces are likely to compound the diversity. Sharper differentiation of the various corporate governance types and the different bases for governance power will be necessary to increase the effectiveness of governance and enable the regulatory processes to respond to reality… But on the other hand, we might expect a convergence of governance processes as large corporations operating globally, their shares traded through global financial markets, are faced with increasing regulatory convergence in company law, disclosure requirements and international accounting standards, insider trading and securities trading rules, and the exchange of information between the major regulatory bodies around the world. (Tricker, 1994: 520)

In this analysis the strength of diversity rather than uniformity becomes apparent, even to the extent there is some convergence of regulation, and it is increasingly likely this will need to be negotiated among regions and countries rather than disseminated from the Anglo-American heartland. ‘There is then value in maintaining international diversity in corporate governance systems, so that we do not foreclose future alternatives and evolutionary possibilities. The argument resembles the argument for biodiversity in species’ (McDonnell, 2002: 18). The importance of diversity for the exercise of choice and creativity is paramount, and reveals the dangers involved in national and international policymaking vigorously advocating a one-size-fits-all prescription for corporate governance (McDonnell, 2002: 19). Indeed, this essential dynamism of corporate governance was fully recognised in the OECD Business Advisory Group’s report at the time of the formulation of the original OECD principles:

Entrepreneurs, investors and corporations need the flexibility to craft governance arrangements that are responsive to unique business contexts so that corporations can respond to incessant changes in technologies, competition, optimal firm organization and vertical networking patterns. A market for governance arrangements should be permitted so that these arrangements that can attract investors and other resource contributors – and support competitive corporations – flourish. To obtain governance diversity, economic regulations, stock exchange rules and corporate law should support a range of ownership and governance forms. Over time, availability of ‘off the shelf’ solutions will offer benefits of market familiarity and learning, judicial enforceability and predictability. (OECD, 1998: 34)

Future trends

Contemplating the future of corporate governance systems is a hazardous business. Each of the systems is facing pressures to change. The long-term stakeholder orientation of the German and Japanese governance systems is under insistent pressure to deliver shareholder value, particularly from overseas investment institutions. However, the market oriented short-termism of the Anglo-American approach is itself being challenged by international, national and community agencies to recognize wider social and environmental responsibilities. The German and Japanese systems are faced with demands for increased transparency and disclosure from both regulators and investors, while Anglo-American corporations are faced with repeated calls for greater accountability from institutional investors and other stakeholder communities.

Bratton and McCahery (2002: 30) recognized four possible outcomes from the present pressures to converge, and the resilient institutional resistance encountered:

- a unitary system as there is strong convergence towards a global system which assembles the best elements of both major governance systems and combines them together (the least likely alternative);

- a universal market based system as anticipated by the Chicago School of financial economists, representing the triumph of the rules based outsider system;

- an improved variety of governance systems in which there is weak convergence, but some learning from each other between the different national systems;

- a set of viable distinctive governance systems, based on distinctive institutional complementarity each having a unique identity and capability.

Contrary to all of the predictions of an early and complete convergence of corporate governance systems, the final two alternatives are the closest to the present state of play, and are likely to be for some time to come, as this differentiated system has a proven robustness and usefulness, reflecting different industrial strengths and strategic directions. The immense capacity of the international finance institutions to continue to drive economic and social change in their own interests should be recognised, and the increasing financialisation of corporations globally disciplined to narrower and narrower financial objectives is a plausible scenario. The continuing threat to the variety and distinctiveness of regional forms of corporate governance and strategy should be recognised. However Anglo-American financial institutions, even if untamed by post-crisis regulation, are under some constraint by the widespread popular demand that they demonstrate greater social responsibility (Clarke, 2010b; Clarke, 2016a). Secondly as presently in China, regional financial systems with different orientations and objectives to the Western banks may exert increasing influence (and indeed Chinese corporations have benefited from this radically different regime in their rapid advance).

Complexity of corporate governance forms

It is likely the campaign to raise standards of corporate governance will continue for some time in all jurisdictions of the world. There will be a strenuous effort to secure commitment to the essential basis of trust identified by the OECD as fairness, transparency, accountability and responsibility. However, this will occur in countries with different cultures, legal systems, and economic priorities and social commitments. This campaign to raise standards of accountability in corporate governance should be distinguished from the intense and numbing assault by international financial interests to impose on the corporations of the world a narrow and self-interested shareholder value ideology which will serve to constrain corporations’ purpose and development.

To assume that all countries will adapt to the same corporate governance structures is unrealistic, unfounded and unimaginative. It is likely that fundamental features of the European and Asian approaches to corporate governance will be maintained, even where the apparatus of market-based corporate governance are formally adopted. Often these differences will be perceived as part of the cultural integrity and economic dynamism of the economy in question. To the extent countries adopt universal principles they will do so within a culturally diverse set of corporate values, structures, objectives and practices. This is part of the evolving and dynamic complexity of corporate life, in which both convergence and divergence can occur simultaneously. As pressures to conform to international standards and expectations increase, the resilience of historical and cultural differences will continue. The business case for diversity is, if anything, even more compelling. There will be a continual need to innovate around new technologies, processes and markets. This will stimulate new organisational and corporate forms, the shape and objectives of which will be hard to predetermine.

Aguilera, R. and G. Jackson (2003) ‘The cross-national diversity of corporate governance: Dimensions and determinants’, Academy of Management Review, 28(3): 447-465.

Aguilera. R., K.A. Desender and L.R.K. de Castro (2012) ‘A bundle perspective to comparative corporate governance’, in T. Clarke and D. Branson (eds.) Sage Handbook of Corporate Governance. London: Sage.

Amable, B., E. Guillaud and S. Palombarini (2012) ‘Changing French capitalism: Political and systemic crises in France’, Journal of European Public Policy, 19(8): 1168-1187.

Avgouleas, E. (2013) ‘Rationales and designs to implement an institutional big bang in the governance of global finance’, Seattle University Law Review, 36: 321-390.

Bebchuck, L.A. and M.J. Roe (1999) ‘A theory of path dependence in corporate ownership and governance’, Stanford Law Review, 52: 127-170.

Branson, D. (2004) ‘The very uncertain prospects of ‘global’ convergence in corporate governance’, Cornell International Law Journal, 34: 321-362.